Q2 2026 Investor Letter

Fellow Investors,

As America celebrated 250 years of freedom, I spent a few days at the beach with nearly 50 extended family members, marking our 27th consecutive year of beach vacation together. Similarly, Michael’s family made its annual pilgrimage to Fair Haven, NY to stay at the lake house that has been in his family since 1966. It has been a good year at KCA, and it was nice to take a few days off and prepare for the second half. We’re thankful for families (and a country) that have built long-lasting traditions, and hope Kingdom Capital can do the same.

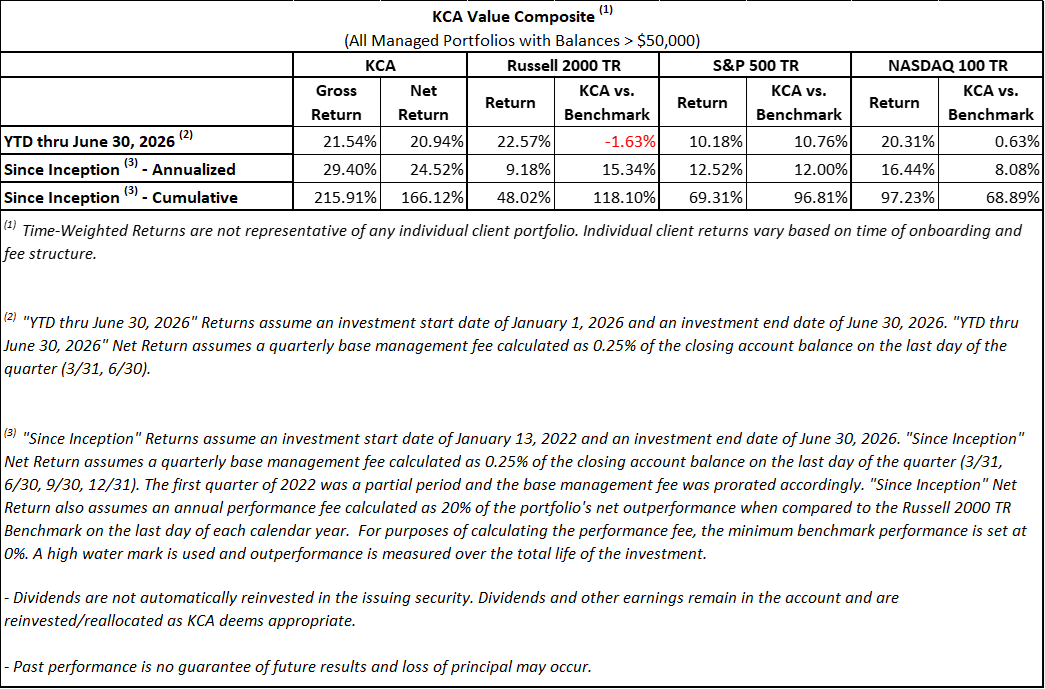

Kingdom Capital Advisors’ KCA Value Composite returned 11.97% net of fees in the second quarter. Year-to-date through June 30, 2026, the composite returned 20.94% net of fees, compared with 22.57% for the Russell 2000 TR, 10.18% for the S&P 500 TR, and 20.31% for the Nasdaq 100 TR.

Since inception in January 2022, we have compounded at 24.52% net annualized versus 9.18% for the Russell 2000 TR, representing approximately 118 percentage points of cumulative net outperformance. Returns vary by account due to rounding, account size, and timing of deposits or withdrawals.

Our top contributors this quarter were Entravision Communications (EVC) and Beasley Broadcasting Group (BBGI). Our largest detractors were Scully Royalty (SRL) and Core Natural Resources (CNR).

KCA Milestone

Q2 brought a new milestone for Kingdom Capital, as it was the first time we filed with the SEC to disclose a 5% position in a single class of stock: June 8th, we disclosed a 7.2% position in Beasley Broadcasting (BBGI) Class A shares. While in Vegas for the Planet Microcap conference a few weeks later, I was able to walk the crowd through an overview of our thesis.

Beasley has been a difficult long-term investment, with the stock down more than 90% from its peak ten years ago. The company got itself into such a debt predicament that their notes were trading hands for 25 to 30 cents on the dollar. One firm saw an opportunity, built a position in their debt, and offered to exchange the notes for new debt at 50% of face value, lowering Beasley’s net debt by nearly $100m. The new debt matures sooner, with an important caveat that if they don’t pay it off the new debt holders will take control of 95% of the outstanding stock.

You may be asking yourself why I find this attractive. We believe the new capital structure creates a strong incentive for the Beasley family to monetize valuable assets to avoid losing control of the business. Based on our estimates, the company’s real estate and radio station assets could support value of up to approximately $200 per share after repayment of outstanding debt, though realizing that value depends on asset-sale timing, execution, and market conditions. With their interests finally aligned with common shareholders, we hope they can reverse the company’s long-term underperformance and do right by investors. Thanks to our active, go-anywhere approach, we were able to establish our position under $6/share in April, before increasing the stake as we gained confidence in the aligned incentives.

While in Vegas, we also visited AKA’s flagship Culture Kings store again, where our observations continued to support our view that consumer demand for the brand remains healthy. For what it’s worth, Mikal Bridges appears to be an enthusiastic customer:

Core Positions

We made a notable re-entry into Entravision (EVC) during Q2 after spending the past year on the sidelines. Our prior thesis centered on the latent value of the company’s broadcast business and spectrum assets. Today, the investment case increasingly centers on Smadex, the company’s ad-tech platform, which generated $34 million of operating income in Q1 and grew revenue more than 200%. Even assuming no further sequential growth in FY26, we believe the market is assigning Smadex a single-digit earnings multiple, while giving limited credit to the company’s spectrum assets. Based on comparable transactions and public-market valuations, we estimate Smadex alone could be worth $15–20 per share, with additional upside if the business continues to diversify its customer base. Walmart just bought a competitor, Vibe, for over $1B, which was doing less than a third of the revenue of Smadex. Peer Liftoff (LFTO) also just came public at a significant premium to Smadex’s valuation.

Core Natural Resources (CNR) also reentered the portfolio after previously being a top holding in 2022 under the Arch Resources banner. Following Arch’s merger with CONSOL Energy, Core owns some of the lowest-cost and highest-quality thermal and metallurgical coal assets in the U.S. We expect Core to generate a meaningful portion of its current market value in cash over the next few years and to deploy that cash toward share repurchases. Recent geopolitical instability has reinforced the importance of energy security and could support sustained demand for coal exports, while eventual reconstruction activity in conflict-affected regions may support steel demand, the end market for Core’s metallurgical coal.

Beyond the new big positions, it was a relatively quiet quarter for our top positions. United Natural Foods (UNFI) and Magnera (MAGN) continue to execute their business plans and trade at cheap valuations. We expect them both to continue to inflect their earnings power higher in the coming quarters, ahead of street expectations. Net Lease Office Properties (NLOP) continues to sell office buildings and move toward a full liquidation, and we expect it to take place at a nice premium to where we recently began adding shares again.

Opportunistic Activity

We remained very active across other names in the portfolio during the second quarter, with profitable trades across QVC, Inc. Preferred Stock (QVCGP), Vital Farms (VITL), DoubleDown Interactive (DDI), and America’s CarMart (CRMT). In each case, we thought the market had over- or underreacted to news and were able to take advantage of the dislocation to generate gains for our investors.

We have a few ongoing opportunistic trades that we hope will also end well for us:

Agility Robotics announced its intended merger with Churchill Capital XI (CCXI), which would make it the first publicly traded humanoid robotics company. While this may sound more thematic than our typical investments, we believe it trades at a meaningful discount to better-known humanoid robotics companies that have received far more investor attention. Agility’s Digit is among the most commercially deployed humanoid robots in the world, with paying deployments at Amazon, Schaeffler, GXO, Toyota, and Mercado Libre. Across nine facilities, it has logged more than 65,000 hours of operation.

While Net Lease Office (NLOP) remains a cornerstone of our portfolio, we dipped into Elme Communities (ELME) at the end of Q2, as their ongoing efforts to sell their final multi-family apartment building hit a snag and the stock sold off aggressively. While we appreciate the frustration from remaining shareholders, we also do not expect a large property like Riverside in Northern Virginia to trade at a double-digit cap rate.

We began building a position in Scully Royalty (SRL) earlier this year after an activist group took over management. The stock was subsequently halted indefinitely in May, temporarily limiting liquidity. If ongoing litigation is resolved, we expect trading to eventually resume, and we estimate the fair value of Scully’s royalty interest is multiple times the price at which the stock was halted. Due to Schwab’s standard reporting treatment for halted securities, client statements may currently reflect this position at little or no value, creating an approximately 2.5% headwind to reported Q2 results.

Closing Thoughts

Our opportunity set remains broader than our available capital, and we expect to remain active in the current environment. We maintain a balanced portfolio of special situations and deep value investments, which we believe positions us well to generate attractive returns going forward. As always, thank you for your continued trust and partnership. Please do not hesitate to reach out with any questions.

Sincerely,

David Bastian

Chief Investment Officer

DISCLOSURES

This document is not an offer to invest with Kingdom Capital Advisors, LLC (“KCA” or the “firm”).

The statements of the investment objectives are statements of objectives only. They are not projections of expected performance nor guarantees of anticipated investment results. Actual performance and results may vary substantially from the stated objectives. Performance returns are calculated by Morningstar.

An investment with the firm involves a high degree of risk and is suitable only for sophisticated investors. Investors should be prepared to suffer losses of their entire investments.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the firm described herein may differ materially from those reflected or contemplated in such forward-looking statements.

This document and information contained herein reflects various assumptions, opinions, and projections of Kingdom Capital Advisors, LLC (“Kingdom Capital Advisors” or “KCA”) which is subject to change at any time. KCA does not represent that any opinion or projection will be realized.

The analyses, conclusions, and opinions presented in this document are the views of KCA and not those of any third party. The analyses and conclusions of KCA contained in this document are based on publicly available information. KCA recognizes there may be public or non-public information available that could lead others, including the companies discussed herein, to disagree with KCA’s analyses, conclusions, and opinions.

Upon request, KCA will furnish a list of all prior securities discussed in our publications within the past twelve months to include the name of each security discussed, the date and nature of each discussion, the market price at that time, the price at which the KCA acted upon the discussion (if at all), and the most recently available market price of each security.

Funds managed by KCA may have an investment in the companies discussed in this document. It is possible that KCA may change its opinion regarding the companies at any time for any or no reason. KCA may buy, sell, sell short, cover, change the form of its investment, or completely exit from its investment in the companies at any time for any or no reason. KCA hereby disclaims any duty to provide updates or changes to the analyses contained herein including, without limitation, the manner or type of any KCA investment.

Positions reflected in this letter do not represent all of the positions held, purchased, and/or sold, and may represent a small percentage of holdings and/or activity.

The S&P 500 TR, Russell 2000 TR, and NASDAQ 100 TR are indices of US equities. They are included for information purposes only and may not be representative of the type of investments made by the firm. The firm’s investments differ materially from these indices. The firm is concentrated in a small number of positions while the indices are diversified. The firm return data provided is unaudited and subject to revision.

None of the information contained herein has been filed with the U.S. Securities and Exchange Commission, any securities administrator under any state securities laws, or any other U.S. or non-U.S. governmental or self-regulatory authority. Any representation to the contrary is unlawful.

This information is strictly confidential and may not be reproduced or redistributed in whole or in part.