Q1 2026 Investor Letter

Fellow Investors,

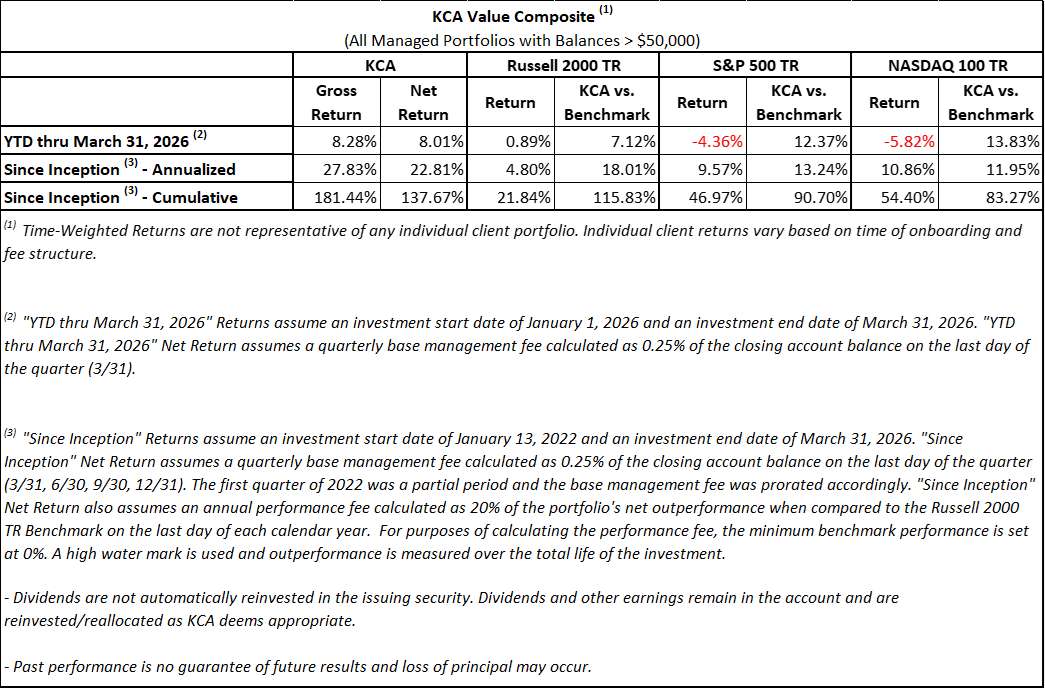

The first quarter of 2026 demonstrated strong performance despite volatility in the broader market driven by ongoing conflict in the Middle East. We feel fortunate that we avoided the AI-driven wipeout in software and watched multiple anticipated catalysts for special situation investments come to fruition. Kingdom Capital Advisors (KCA Value Composite) returned 8.01% (net of fees) in the first quarter, vs. 0.89% for the Russell 2000 TR, -4.33% for the S&P 500 TR, and -5.82% for the NASDAQ 100 TR.

Since inception in January 2022, we have compounded at 22.81% net annualized versus 4.80% for the Russell 2000, representing cumulative outperformance of over 115%. Returns vary by account due to rounding, account size, and timing of deposits or withdrawals.

Our top contributors this quarter were United Natural Foods (UNFI), Energous Corporation (WATT) and Alliance Entertainment (AENT). Our largest detractors were Magnera Corporation (MAGN), Mount Logan Capital, Inc. (MLCI) and WW International (WW).

Active Management

As discussed in prior letters, our special situation strategy can appear underwhelming in strong bull markets but tends to provide meaningful downside protection and uncorrelated returns during more volatile periods. The start of 2026 has reinforced this dynamic.

The first half of 2025 marked our most challenging period since inception, with the composite declining by over 10%. Since that trough, we have rebounded nearly 40% over the subsequent nine months. We appreciate your continued trust and patience through periods of volatility.

We were active during the quarter and exited several positions after achieving our targeted returns:

TSS, Inc. (TSSI): Following a ~50% decline due to delayed rack integration volumes (highlighted in our Q4 letter), the company’s results in March confirmed a successful facility ramp. The stock doubled from its lows, and we exited the position with gains, capping our third profitable cycle in this name over the past two years.

Energous (WATT): A historically awful consumer products business, WATT has pivoted to supply chain tracking solutions. We initiated a position when the company’s market capitalization approximated its cash balance, reflecting minimal expectations for the business. As the company secured meaningful contracts (including Walmart), the stock rerated significantly, rising from our ~$8 entry to over $20 at its peak. Following a dilutive capital raise by management, we exited the position with a return exceeding 100% over approximately two months.

SunOpta (STKL): After meeting management at the ICR Conference, we developed conviction in the company’s competitive positioning in shelf-stable plant-based milk and fruit snacks. We began building a position with the expectation it could become a core holding. However, the company agreed to be acquired for $6.50 per share shortly thereafter. While we would have preferred a larger position, the investment generated a return of nearly 50% in less than one month.

We also generated gains in shorter-duration positions, including Ziff Davis (ZD) (driven by a business divestiture) and Kodak (KODK) (supported by improving profitability and balance sheet strength). These situations reflect our belief that it is worth our time to pursue opportunities in less-followed areas of the market.

Core Positions

A notable addition this quarter is Alliance Entertainment (AENT), where we built a significant position following a post-earnings dislocation. Alliance distributes physical media (DVDs, vinyl, and CDs) to over 35,000 retail locations and fulfills online orders for major retailers. While traditional physical media consumption has declined, the category has evolved toward collectibles, supporting renewed growth in select segments.

Key elements of our thesis include:

Strong insider alignment, with over 90% ownership by insiders and employees

Estimated run-rate EBITDA of ~$60 million, implying ~6x EV/EBITDA with growth potential

Exclusive distribution agreement with Paramount, which has significantly boosted earnings in the past year. I am optimistic Paramount’s recent buyout offer for Warner Brothers (WBD) will result in Alliance securing an even larger catalogue, which could push EBITDA closer to $100m run-rate. They are also ramping an exclusive distribution agreement with Amazon/MGM beginning in January 2026.

Benefits from record-breaking Mach releases from Harry Styles, BTS, and Bruno Mars. Styles sold more Vinyl in the first week than any male artist since at least 1991.

Capital structure reminiscent of our former holding Abacus Global (ABX), which had significant capital locked up in their SPAC warrants. Alliance has over $110m of capital accessible if their stock trades above $11.50 between now and February 2028, which would turbocharge their ability to grow via acquisition in their niche, and put their balance sheet in a net cash position.

Elevated short interest and high borrow costs (50–75%), which we view as unsustainable over time

We continue to hold a large position in Net Lease Office Properties (NLOP) as the company monetizes its remaining suburban office assets. While the sale price of its largest asset (KBR) was below expectations, we believe the remaining portfolio still offers over 20% of remaining upside, with resolution likely by year-end. Notably, cumulative dividends received have already exceeded our initial cost basis.

We remain constructive on United Natural Foods (UNFI), following its December investor day. The stock has rebounded nearly 50% from recent lows, supported by improving sentiment and early signs of shareholder-friendly capital allocation, including share repurchases. The company continues to trade at an attractive free cash flow yield (>10%), with multiple levers for earnings growth, including margin expansion and declining interest expense.

Magnera (MAGN) has retraced gains following its late-2025 rally, with market concerns focused on rising commodity costs. However, management has reiterated guidance and emphasized hedging strategies that mitigate input cost risk. While near-term performance has been frustrating, our fundamental view remains unchanged. I spent over an hour walking through our thesis on the Value Cville podcast back in January:

https://podcasts.apple.com/us/podcast/episode-11-david-bastian/id1835989398?i=1000745770562

Finally, Enviri (NVRI) continues to progress toward the sale of its Clean Earth segment, which we expect will return a substantial portion of our invested capital in cash. We believe the remaining business will be well-positioned post-transaction and will provide additional updates in future letters.

Closing Thoughts

Our opportunity set remains broader than our available capital, and we expect to remain active in the current environment. We maintain a balanced portfolio of special situations and deep value investments, which we believe positions us well to generate attractive returns going forward. As always, thank you for your continued trust and partnership. Please do not hesitate to reach out with any questions.

Sincerely,

David Bastian

Chief Investment Officer

DISCLOSURES

This document is not an offer to invest with Kingdom Capital Advisors, LLC (“KCA” or the “firm”).

The statements of the investment objectives are statements of objectives only. They are not projections of expected performance nor guarantees of anticipated investment results. Actual performance and results may vary substantially from the stated objectives. Performance returns are calculated by Morningstar.

An investment with the firm involves a high degree of risk and is suitable only for sophisticated investors. Investors should be prepared to suffer losses of their entire investments.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the firm described herein may differ materially from those reflected or contemplated in such forward-looking statements.

This document and information contained herein reflects various assumptions, opinions, and projections of Kingdom Capital Advisors, LLC (“Kingdom Capital Advisors” or “KCA”) which is subject to change at any time. KCA does not represent that any opinion or projection will be realized.

The analyses, conclusions, and opinions presented in this document are the views of KCA and not those of any third party. The analyses and conclusions of KCA contained in this document are based on publicly available information. KCA recognizes there may be public or non-public information available that could lead others, including the companies discussed herein, to disagree with KCA’s analyses, conclusions, and opinions.

Upon request, KCA will furnish a list of all prior securities discussed in our publications within the past twelve months to include the name of each security discussed, the date and nature of each discussion, the market price at that time, the price at which the KCA acted upon the discussion (if at all), and the most recently available market price of each security.

Funds managed by KCA may have an investment in the companies discussed in this document. It is possible that KCA may change its opinion regarding the companies at any time for any or no reason. KCA may buy, sell, sell short, cover, change the form of its investment, or completely exit from its investment in the companies at any time for any or no reason. KCA hereby disclaims any duty to provide updates or changes to the analyses contained herein including, without limitation, the manner or type of any KCA investment.

Positions reflected in this letter do not represent all of the positions held, purchased, and/or sold, and may represent a small percentage of holdings and/or activity.

The S&P 500 TR, Russell 2000 TR, and NASDAQ 100 TR are indices of US equities. They are included for information purposes only and may not be representative of the type of investments made by the firm. The firm’s investments differ materially from these indices. The firm is concentrated in a small number of positions while the indices are diversified. The firm return data provided is unaudited and subject to revision.

None of the information contained herein has been filed with the U.S. Securities and Exchange Commission, any securities administrator under any state securities laws, or any other U.S. or non-U.S. governmental or self-regulatory authority. Any representation to the contrary is unlawful.

This information is strictly confidential and may not be reproduced or redistributed in whole or in part.